A day laden with significant events unfolded as the Consumer Price Index (CPI) release provided insight into inflation trends, the European Central Bank (ECB) meeting took center stage, and various asset classes exhibited notable movements. The CPI data, although slightly hotter than expected, failed to significantly sway expectations regarding the Federal Open Market Committee's (FOMC) decision on interest rates next week. The prevailing sentiment is that the FOMC will likely refrain from rate hikes, with a potential tightening move in November still perceived as a 50-50 proposition.

Treasuries headed into the CPI data with a bias towards upside risks, resulting in a spike in yields following the 0.6% rise in the headline CPI and a 0.3% gain in the core CPI. This translated to year-on-year rates of 3.7% and 4.3%, respectively. However, yields swiftly retreated, ending the session on a stronger note amid short-covering activity.

Asian stocks saw modest gains as investors shrugged off stronger-than-expected US inflation figures and turned their attention to the impending ECB decision.

ECB Meeting and Rate Hike Expectations

The ECB meeting, a highlight of the day, saw reports suggesting that updated staff projections would push the 2023 inflation forecast above 3%, fueling expectations of another 25 basis point hike. While a hawkish pause would not have been surprising, some analysts saw a slightly higher likelihood of the ECB taking action this week, particularly considering the anticipated upward revision to inflation forecasts and the recent surge in energy prices.

In the foreign exchange markets, the USD Index stood at 104.60. EURUSD exhibited mixed performance but trended lower during the European session, trading at 1.0733, down from 1.0754, while USDJPY maintained its position above the 147.00 mark, with an eye on 148.

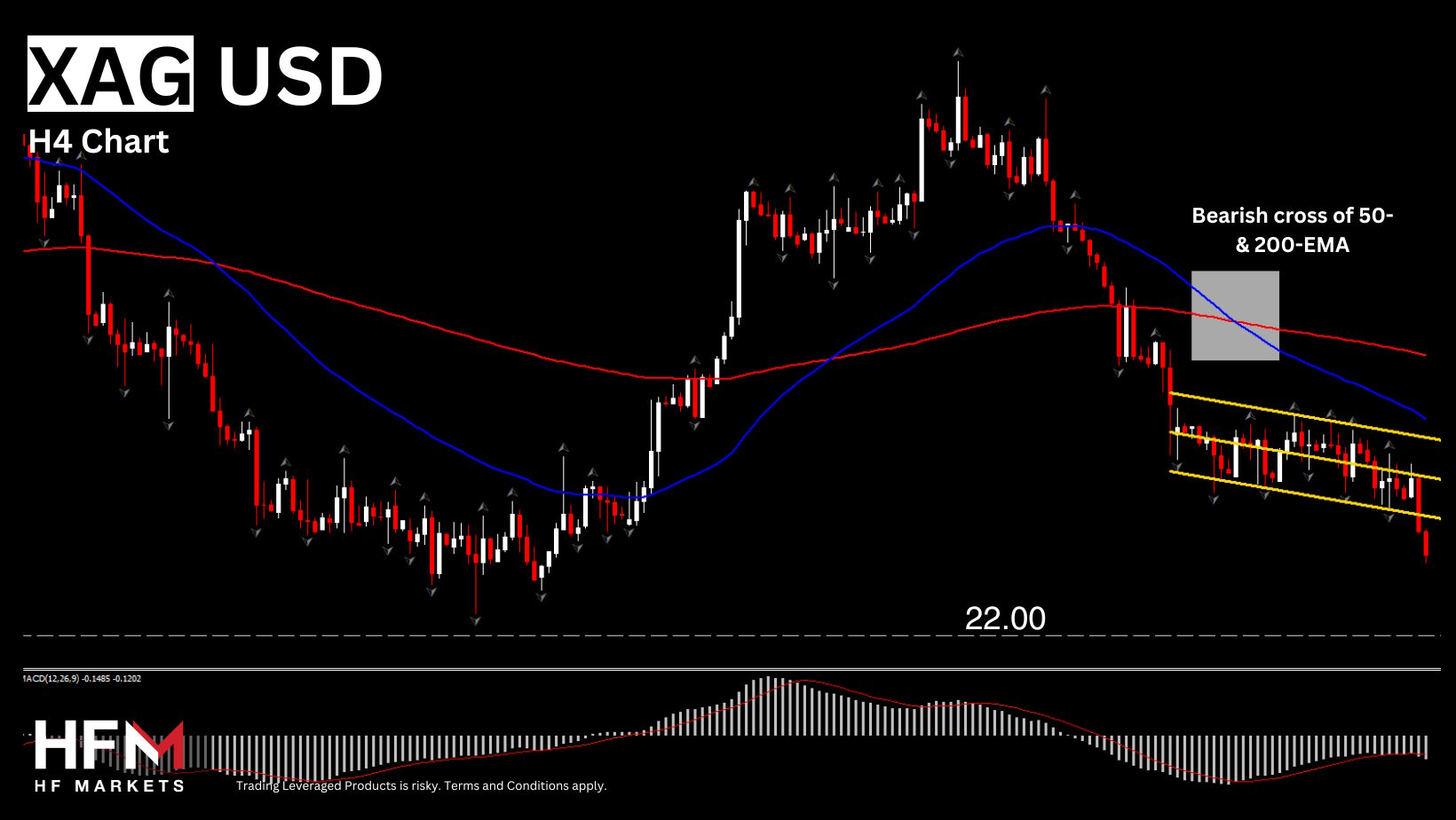

Key Mover: Silver (XAGUSD)

Silver (XAGUSD) experienced a 1.18% decline, breaking a five-day range and extending its downward trajectory in September. Attention now turns to support levels at 22 and 21.

Stock Movements

Stock markets witnessed various movements, with the JPN225 surging 1.4% to reach 33,168.10. The US500 edged upward to 4534, US100 reached the August ceiling, and the US30 faced resistance above the 35,000 level. In the US500, airline stocks faced notable losses as some companies warned of profit declines due to rising costs. United Airlines saw a 3.8% decline, while Delta Air Lines dropped by 2.8%. Conversely, tech giants like Amazon gained 2.6%, Microsoft rose 1.3%, and Nvidia advanced by 1.4%. Moderna reported promising results from a flu vaccine trial, leading to a 3.2% rally in its stock.

- Commodity Market Focus. In the commodities arena, oil remained well-supported, with attention centered on the possibility of sustained supply constraints throughout the year. USOIL was priced at $88.60, rebounding from its low of $87.60.

- Upcoming Highlights. The day's calendar included the ECB rate decision and press conference, as well as US Retail Sales and Producer Price Index (PPI) data.