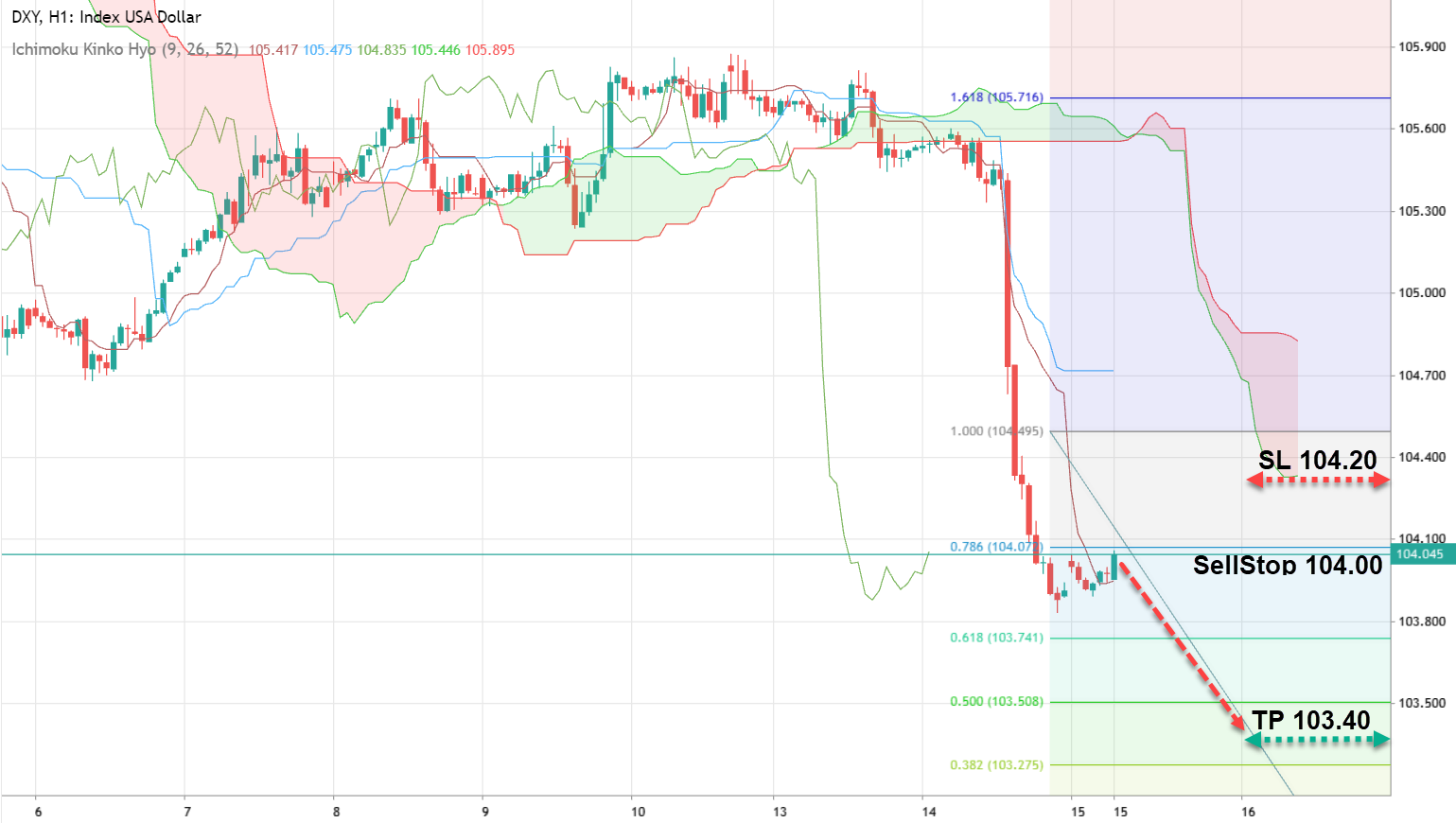

The US Dollar Index (DXY) is currently trading around the 104.00 mark, as investors are closely analyzing the implications of the October Consumer Price Index (CPI) report. The report indicated a more significant slowdown in inflation than anticipated, with the headline CPI figure coming in at a flat 0.0% on a monthly basis, and dropping from 3.7% to 3.2% year-over-year, slightly below the expected 3.3%. Core inflation, which excludes volatile food and energy prices, also showed a decrease from 4.1% to 4.0% year-over-year.

This deceleration in inflation has fueled speculation among investors that the Federal Reserve might pause or slow down its interest rate hikes, a scenario that could exert downward pressure on the US dollar. The declining inflation figures have also impacted the US debt market, triggering a selloff that contributed to the dollar's weakening.

Given these market conditions, a trading strategy involving a sell stop at 104.00 with a target price (TP) of 103.40 and a stop loss (SL) at 104.20 could be considered.

USD/JPY: External Factors and Speculation of Government Intervention

The USD/JPY pair is experiencing a downward trend, currently trading at around 105.50. In the absence of significant domestic economic releases, the yen's movements are largely influenced by external factors. Japanese Finance Minister Shunichi Suzuki's recent comments have drawn attention. He stated that the government would continue to monitor the foreign exchange market and respond as necessary, though he stopped short of explicitly mentioning currency interventions. This cautious stance, coupled with the weakening dollar post-inflation report release, has placed the pair under selling pressure.

A potential trading approach could be a sell stop at 150.50, with a TP at 149.50 and an SL at 150.80, taking into account the current market dynamics and the possibility of government intervention.

BRENT: Consolidation and Positive Outlook

Brent crude oil is consolidating near $83 per barrel, finding support from various positive developments. The International Energy Agency (IEA) has revised its oil demand forecast for this year upwards, from 2.3 million barrels to 2.4 million barrels per day. Similarly, OPEC analysts have raised their demand outlook for crude oil. Additionally, the US Department of Energy’s announcement of plans to purchase 1.2 million barrels of oil for reserve replenishment has bolstered market sentiments.

The upward trend in oil prices is further supported by robust data from China, indicating a continued economic recovery. China's industrial production rose by 4.6%, underscoring the country's status as the world's largest oil importer. Considering these factors, a continued rise in oil prices seems plausible.

Investors might consider a buy stop at 83.00, targeting a TP at 85.00 and setting an SL at 82.40, in light of the positive demand outlook and supportive market fundamentals.