After the Federal Reserve's hawkish stance, all eyes are now on the core Personal Consumption Expenditures (PCE) index, the Fed's preferred gauge of inflation, due to be released on Friday at 12:30 GMT. While the Fed decided to maintain steady rates last week, the tone of its policymakers was notably hawkish, signaling a higher rate trajectory compared to June. This shift in sentiment includes projections of another quarter-point rate hike by the end of the year and only two rate cuts anticipated in 2024. Specifically, officials foresee rates at 5.1% by 2024, up from the 4.6% projection in June.

However, market sentiment did not align entirely with the Fed's projections. Investors have priced in only a roughly 50% probability of a final rate hike, suggesting that rates may end 2024 at 4.7%. This implies room for adjustment should data continue to indicate a robust US economy, potentially providing further momentum to the US dollar.

As market attention shifts to the upcoming data, this week's focus is primarily on Friday's core PCE index. This inflation metric holds significance for the Fed, even though it may not carry as much market-moving weight as other indicators. Alongside the core PCE index, data on personal income and spending will also be released, while Thursday will see the unveiling of the final GDP figures for Q2 and initial jobless claims for the preceding week. Regarding GDP, it is likely to draw little attention as existing models already offer insights into Q3's economic performance. The Atlanta Fed GDPNow suggests an impressive 4.9% growth rate, while the New York Nowcast indicates approximately 2.3% growth. Despite the variance, both models point to a robust economic performance, aligning with the Fed's "higher for longer" approach.

Forecasts for Friday's core PCE index indicate a slowdown, supported by the cooling of the core Consumer Price Index (CPI) for the month. Even if this underlying inflation metric decelerates, it is expected to remain above the Fed's 2% target. Additionally, with a resilient economy and rising oil prices, the risk of a rebound in the coming months remains plausible.

In terms of personal spending, expectations are for a slowdown, corroborating the slight dip in retail sales for the month and signaling reduced consumer demand. Although income is anticipated to have accelerated, the deceleration in average hourly earnings for August leans towards a downside risk.

The dollar may experience a minor retracement if data suggests ongoing cooling of inflation in the US. Nevertheless, this retreat is unlikely to signal the end of the dollar's uptrend. As long as economic data continues to support the view that the US economy is outperforming other major economies, the dollar is expected to remain strong. Alongside the "higher for longer" narrative, the dollar's appeal as a safe haven amid challenges faced by the Chinese economy, the Eurozone, and the UK, remains strong, driven by higher US interest rates.

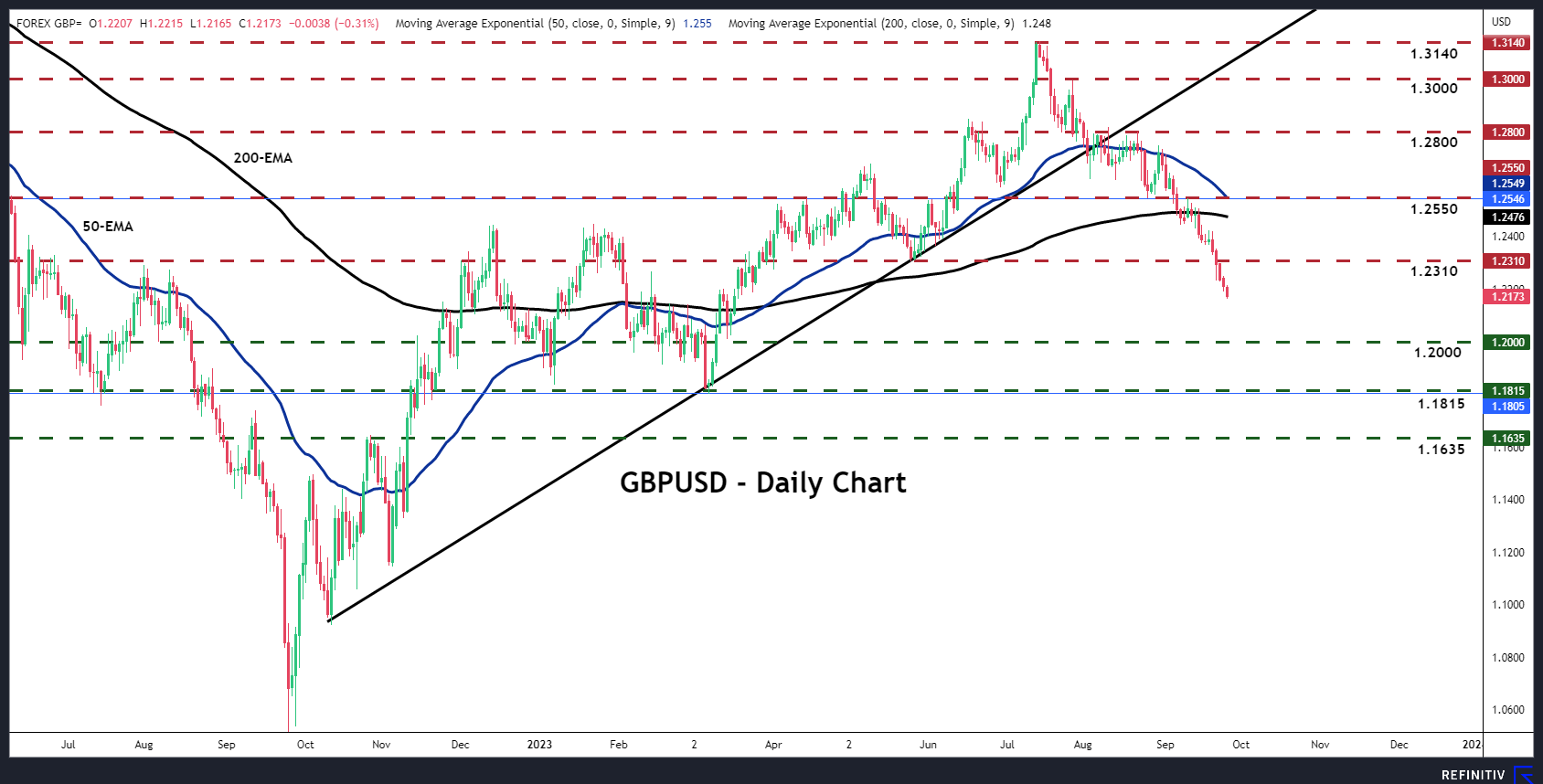

In the forex market, pound/dollar (GBPUSD) stands out as a pair that could continue to face pressure. The Bank of England's decision to remain on the sidelines, with a 75% probability of no action in November, suggests the potential for further dollar strength.

The GBPUSD pair has been sliding since mid-July, and following the BoE's decision last week, it breached the key zone of 1.2310, possibly confirming a bearish trend reversal on the daily chart. This decline may pave the way for a test of the psychological round number of 1.2000, followed by the low of March 15 around 1.1815. On the upside, a return above 1.2310 is unlikely to shift the outlook to a positive one; it may merely restore a neutral stance. To establish an uptrend for this pair, a break above the key barrier of 1.2800 may be necessary.