With the RBA meeting in play on Tuesday (14:30 AEST), here's a few variables traders can look at to assess the skew of risk. As always, there's many moving parts, but could the RBA deliver a surprise? Fundamentals supporting the USD - AUDUSD 6 and 12-month forward rates sit at 26 and 44 points respectively – so carry on rolling forward rates modestly favours USD longs. We also see US 2 year Treasury yields commanding a 62bp premium over Aussie 2yr bonds.

Here are a few core considerations

- Rates pricing – There is currently a 0% chance of a hike for this meeting, but we see 170bp (6.8 hikes) priced for end-2022 and 320bp (c. 13 hikes) for end-2023.

- Interest rate markets are pricing the first hike and lift-off for the June meeting, although the case for a 15bp hike earlier to get the cash rate to 25bp has risen – will the RBA statement go anyway to meet these expectations

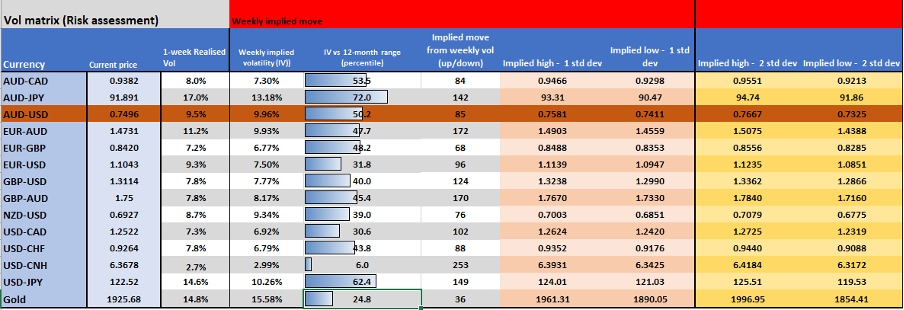

- AUDUSD 1-week implied vol at 9.96% (from Friday’s close) - this is the 50th percentile of the 12-month range – the implied move over the week is 86-pips – this suggests a trading range of 0.7581 to 0.7411 (with a 68.2% level of confidence) and 0.7667 to 0.7325 (95% level of confidence). Whilst there are obviously other drivers, the market is not expecting any glaring surprises from this meeting – could they be proved wrong?

- AUDUSD 1-week call volatility trades at a 0.89 discount to 1-week put vol – this skew is the 59th percentile of the 12-month range – on balance, the market feels if there is a move the risks are symmetrical.

Supporting the AUD - AUD terms of trade are moving higher vs US ToT. We also see a steeper relative Aussie curve and Aus 10yr real yields hold a 77bp premium to US 10yr real rates. The ASX200 is also outperforming the S&P 500 (currency hedged).

- Technicals - On the daily price holds a short-term consolidation range of 0.7540 to 0.7457 – which way does it break? An upside break suggests a potential target of 0.7683 (138% fibo extension of 0.7165 to 0.7540 rally).

- Positioning – retail traders are skewed short AUDUSD (we see 73% of all open positions held short, 74% on AUDJPY) – on the CFTC report, leveraged funds hold a 25,878-contract short position, asset managers are short 2,574 contracts but have been reducing short – so retail, leveraged and real money all still structurally short AUD.

- Other key Aussie events for the dairy – RBA financial stability report (8 April), Aussie employment report (4 April), Q1 CPI (27 April), May RBA meeting (3 May), Q1 wage price index (18 May), Federal election

At some stage the RBA seem destined to move towards the market – could it be this meeting?