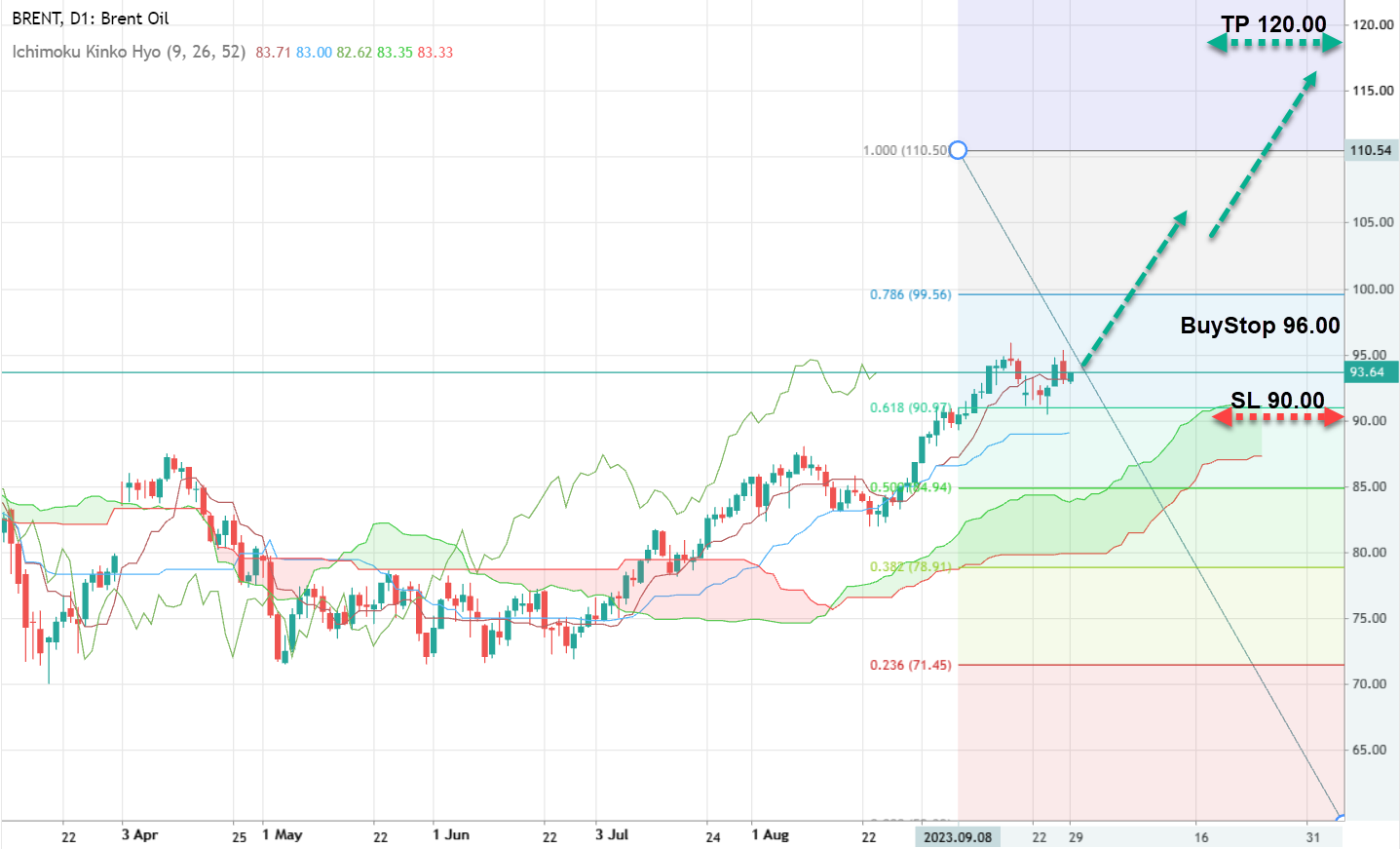

The third quarter of 2023 illuminated a favorable path for the oil industry, as Brent crude experienced a price increase from $75 to $95 per barrel, marking a 25% rise. Bolstering this price momentum were the predictions of a looming deficit in global oil supplies. OPEC+ data for Q3 reported a global shortfall of 1.8 million barrels daily. As we delve deeper, these figures project an even bleaker scenario, with the supply-demand gap anticipated to exceed 3 million barrels daily. Such predictions aren't mere speculations, given the recent decision by Saudi Arabia and Russia to prolong their output cuts until the year's end. Collectively, this means a further 1.3 million barrels will be absent from the market daily.

Global fuel demand, in contrast, is witnessing an upswing, driven by the steady revival of the world economy. With the OECD enhancing its economic growth forecast for 2023 to 3.0% from a prior 2.7%, OPEC analysts project oil demand to rise by 2.4 million barrels daily this year, followed by a 2.2 million barrel increase in 2024.

Haitham Al-Ghais, OPEC's Secretary-General, emphasized a potential global supply crisis. He highlighted that despite fossil fuels comprising over 80% of the global energy blend, the pressure against investing in oil and gas projects owing to environmental reasons could lead to a supply dilemma. IEA analysts have suggested the peak demand for oil, coal, and natural gas could be around 2030.

Unless steps are taken to develop more reserves, the impending deficit might be cataclysmic for the global economy, potentially driving Brent prices above $150 per barrel. Furthermore, China, as the leading global oil importer, has seen a resurgence in demand due to economic revitalization measures. Data indicates China's industrial production increased by 4.5% in August, indicating potential growth in fuel consumption. For investors, this data presents an opportune moment to hold onto long positions in Brent till the end of the year.

Gold’s Resilience Amid Market Fluctuations

Q3 2023 found gold stabilizing near the $1,900 per ounce range, with the metal showing remarkable resilience against the backdrop of rising U.S. bond yields and a robust dollar. Historically, higher U.S. interest rates led to increased bank deposits, drawing conservative investors away from precious metals. Additionally, government bond yields, seen as a secure investment, experienced growth. Consequently, gold prices faced pressure, dropping to as low as $1,886. However, with the world's major central banks adopting a more neutral stance in August, real assets, previously overshadowed, showcased a strong potential for resurgence.

Given the Federal Reserve’s likely conclusion of its current tightening cycle and signs pointing towards a peak in the U.S. dollar’s strength under the current macroeconomic scenario, it’s plausible that investors might shift their focus towards gold. Consequently, gold might edge closer to the $2,000 resistance mark by the end of 2023.

Euro's Struggle Amidst Economic Challenges

The EUR/USD pairing reflected a somber tone as Q3 2023 concluded, further plagued by deteriorating economic conditions in the Eurozone. Key factors such as the Eurozone’s tepid GDP growth of 0.1% in Q2 and the drop in industrial production have stirred concerns. The European Commission’s decision to lower its growth forecasts for the upcoming years only added to these apprehensions. A notable factor dampening Europe’s economic prospects is high inflation, which has impacted consumer activity. With oil prices on the rise since August, this trend may persist through the winter.

However, even as the ECB increased interest rates in September, it failed to instill confidence in euro advocates. With the U.S. Federal Reserve still considering another rate hike in November, the euro's position could further diminish, potentially causing the EUR/USD pair to finish below the 1.0500 support level by 2023's end.

USD/JPY: Speculations Surrounding the Yen

The USD/JPY pairing remains a topic of fervent discussion, with speculations rife about potential changes in Japan's monetary policies and potential interventions by the Bank of Japan. Although Bank of Japan Governor Ueda hinted at a possible departure from the prolonged negative interest rate regime, the September meeting saw no significant change in this stance. Japan’s inflation metrics, which remain below the desired target, further underscore the necessity for continued stimulus.

Given this context and the Bank of Japan's unique stance among developed economies, the USD/JPY pair touched significant highs, renewing debates about potential currency interventions. Should this trajectory continue, the Bank of Japan might need to step in, thereby providing investors a potential window for short positions on the USD/JPY pairing with long-term perspectives.